Playing Ecuador’s Mining Potential: Cornerstone Capital Resources

SPONSORED CONTENT: The Alpala deposit will become Ecuador's largest copper and gold mine

TSXV-listed Cornerstone Capital Resources (stock symbol “CGP”) was a first mover in Ecuador. It acquired the Cascabel copper-gold porphyry property in 2011, brought SolGold in as funding partner under a farm-in arrangement in 2012, and was project operator through to the discovery drill hole in February 2014, transferring operatorship over to SolGold in September 2014. The Alpala deposit on the Cascabel concession will become Ecuador’s largest mine, and one of the world’s most important copper producers, when it begins production in 2029. It also contains more gold resources than Ecuador’s largest current gold mine, Fruta del Norte.

Cornerstone Capital Resources

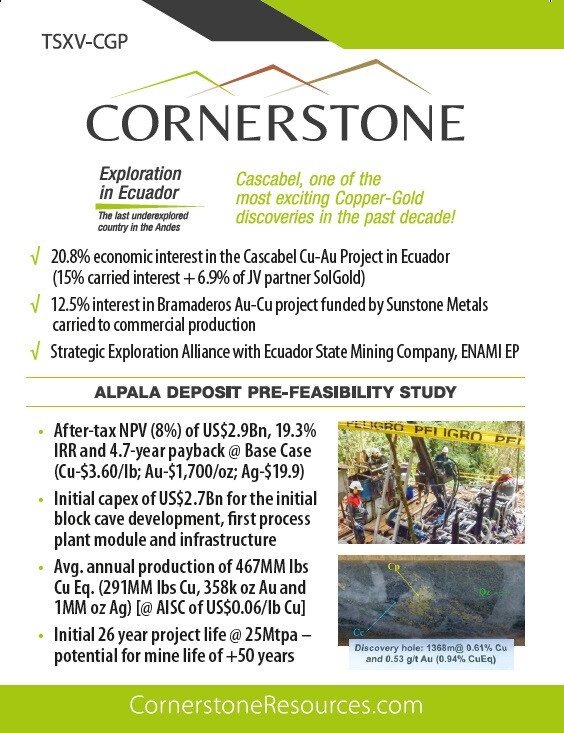

Cornerstone retains a 15% direct stake in Cascabel carried (financed) by SolGold to completion of a bankable feasibility study and repayable out of Cornerstone’s share of dividends or earnings from a mine at Libor plus 2%, plus 6.9% of the shares in SolGold, for a combined project interest of 20.8%.

The recently completed Pre-Feasibility Study (PFS) shows: (1) an after-tax NPV (@ 8% discount rate) of US$2.9billion, 19.3% IRR and 4.7-year payback @ Base Case (Cu-$3.60/lb; Au-$1,700/oz; Ag-$19.9); (2) an initial capex of US$2.7billion for the initial block cave development, first process plant module and infrastructure; (3) average annual production of 467MM lbs copper equivalent (291MM lbs Cu, 358k oz Au and 1MM oz Ag) @ an all-in sustaining cost of US$0.06/lb Cu; and (4) an initial 26 year project life @ 25Mtpa, with the potential for a mine life of >50 years.

The project has already attracted investment from majors such as Newcrest and BHP Billiton, BHP having a 13.6% and Newcrest a 13.5% stake in SolGold (or ~11.5% of Cascabel each) so Cornerstone’s strategic 20.8% interest makes it an attractive acquisition target says H. Brooke Macdonald, Cornerstone’s CEO: “There are simply not enough copper projects in the development pipelines of major mining companies to meet the anticipated demand for electric vehicles and low-carbon electrical infrastructure by 2030-2050, and underinvestment by the majors in early-stage copper exploration means to maintain their production profiles and market valuations they will need to buy reserves - by acquiring juniors like Cornerstone and SolGold - to replace reserve depletion, so we anticipate a frenzy of M&A activity for existing copper projects like Cascabel as well as companies willing to fund drilling in potentially large porphyry system environments in good jurisdictions like Ecuador.”

Macdonald expects Cornerstone Capital Resources to be bought out within the next 12 months. At present the company’s market cap stands at around $119million with a share price hovering around CAD$3.19. Yet analysts believe the recent pre-feasibility study for Cascabel means Cornerstone is worth much more. A conservative estimate from David Davidson, the Senior Analyst, at Paradigm Capital, has a $6.50 target on the stock, which he rates as a speculative buy.

Other opportunities

But while most of the attention is focused on Cascabel, Macdonald points out that Cornerstone’s other concessions could be spun out into a separate SpinCo. Backed by current Cornerstone VP Exploration and Ecuador country manager, Yvan Crepeau, who has worked with him since the early days at Cascabel, Macdonald believes there is plenty of potential in the rest of Cornerstone’s concessions.

Back in 2015, when Ecuador was still a pariah in global mining circles, following the 2007 Mining Mandate (moratorium) and high-profile departure of Kinross in 2014, Cornerstone signed a letter of intent with state miner, Enami EP. That was upgraded to a formal strategic exploration alliance (SEA) in 2016, with the idea that alliance partners could use Cornerstone’s proprietary geological database, and knack for generating prospects and drill targets as demonstrated at Cascabel, to identify concessions for Enami to acquire for the benefit of the SEA to be funded by Cornerstone with Cornerstone having the option to earn up to an 84% interest and Enami retaining a 16% carried interest. The SEA is currently exploring the Espejo block of four concessions in NW Ecuador just to the east of Cascabel.

“Espejo is still at an early stage”, says Crepeau. “Surface exploration work is almost completed. Preliminary drill targets are defined and being refined using 3D modelling, while the permitting process is ongoing.” But when it comes to drilling, Cornerstone will bring in another company, just like it did with Cascabel. “Cornerstone is a prospect generator following the joint venture model, so drilling requires us to secure a funding partner”, says Crepeau, “ideally a major mining company with the capacity to develop large porphyry deposits as identified on these properties.”

The main draw will be the excellent geology. After all, Crepeau and Macdonald, together with partner SolGold, were involved in one of Ecuador’s biggest copper and gold discoveries. But the partnership with Enami is also a plus, says Macdonald. “It gives us better social acceptance by communities and local authorities. We also have the use of some of Enami’s heavy equipment to support infrastructure and road construction and maintenance in the project areas.” Enami has had a rocky start since being created on New Year’s Eve in 2009 by former president Rafael Correa, with a string of CEOs. But Enami’s progress with Espejo is starting to prove the doubters wrong. “We are encouraged by the cooperation we have received from Enami”, says Macdonald.

Julian Agurto, the first mining professional to head Enami, is optimistic about the company’s future. “Enami EP offers many competitive advantages, among them we can highlight the fact it has priority in requesting areas with great geological potential. That makes us a natural partner for international mining companies that want to develop projects in Ecuador. Another advantage is that we have established a good relationship with the communities. Indeed, they are allies in the development of mining activities. We have invested time and money in strengthening community relations, as we know that their help is indispensable to develop our projects.”

Agurto believes these strategic alliances will soon yield tangible results. “The strategic alliances are positive. To give an example, we maintain a collaboration agreement with Cornerstone Capital Resources, the operator in the Espejo mining project, located in the province of El Carchi. Together we promote the community relations through specific agreements with the municipalities to improve road access, build sporting facilities and other works that allow us to improve the quality of life of the inhabitants. In that sense there are more than 3,000 families in the zone of direct and indirect influence of the project that have benefited.”

Cornerstone also owns 12.5% of Bramaderos, a gold-copper porphyry in Southwest Ecuador that is conveniently sited next to the Pan American highway. Cornerstone’s stake will be carried by majority partner, Sunstone Metals, through to the start of production, giving Cornerstone investors exposure into yet another potential Ecuadorian mega project. As Paradigm’s Davidson noted in his research note: “While Cascabel is currently the value driver for Cornerstone, Bramaderos and the remaining portfolio hold significant exploration upside for the company moving forward, CGP is well positioned to continue to unlock value across its portfolio.”