Interview with Edwin Rojas, President of the Central Bank of Bolivia

BCB President, Edwin Rojas, says the country's macroeconomic stability and growth potential outweigh any dollar shortage fears...

This interview is part of our Latin American central bank special report...

What are the strengths of the Bolivian economy?

Edwin Rojas: There are a mix of elements that allow us to show the strengths of the Bolivian macroeconomy. The current government has worked for a long time to maintain Bolivia’s economic sovereignty. We don’t sign agreements with multilateral organisations that force us to set economic rules, such as fiscal policy or the exchange rate. Instead, we have imposed our own fiscal and monetary self-discipline. Bolivia follows a social, community, productive economic model that doesn’t just aim to grow GDP but also redistributes wealth.

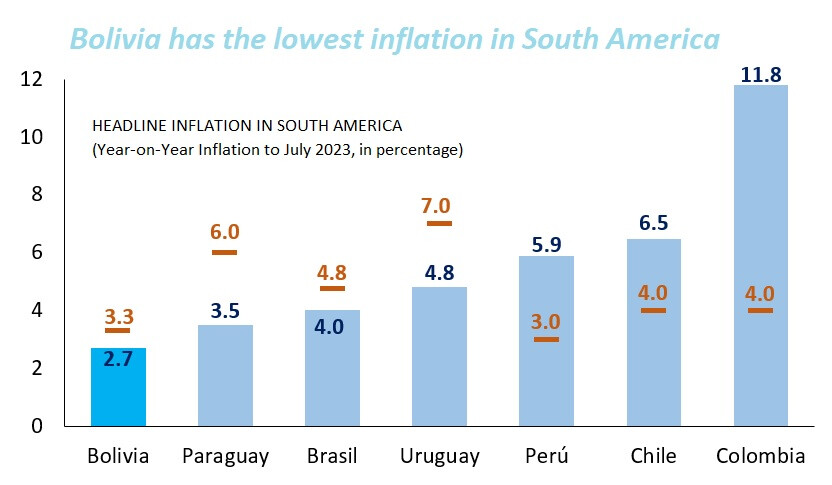

One of our biggest achievements has been to de-dollarize the economy, so nowadays almost 100% of banking loans are denominated in local currency, while 80% of banking deposits are also in bolivian currency. Another great achievement is that we have one of the lowest rates of inflation in the world. We control inflation by coordinating fiscal and monetary policy. It helps that we are independent of the multilateral financial agencies. We are a member of the IMF but we don’t have a programme with it. That means we can run our economy in the best interest of the Bolivian people.

The solidity of our financial system is another strength. In May this year, there was a liquidity problem at the fourth-largest bank in Bolivia. However, the bank was intervened and thanks to different measures it was possible to avoid contagion to the rest of the financial system in a timely manner. Indeed, in June the non-performing loan ratio in Bolivia was 2.7% compared to a Latin American average of 3.5%. This shows how solid our financial system is.

Bolivia’s natural gas production is declining; is that an economic challenge?

ER: If you look at Bolivia’s economic history, we have typically relied on commodities. At one point we were a major tin producer, then we were massive in silver and for the last twenty years it has been gas. The difference with gas is that we successfully nationalised production in 2006, which allowed us to maximise the benefits for the people. For example, we have invested heavily in infrastructure. But now it seems like the gas cycle will come to an end, so we are diversifying our sources of export earnings.

President Luis Arce has overseen an active process of industrialisation, which means the state will not just depend on one product. In addition to manufactured goods, Bolivia has huge reserves of lithium. Indeed, our lithium reserves have a value 75-times greater than our GDP, so the economic impact of developing them would be huge. Another important resource for us is zinc, which is a crucial energy transition material. We believe that next year we will see new zinc mines start operating in Bolivia. We also have significant quantities of gypsum, which we will begin to produce with our first gypsum plant by the end of the year. So, you are looking at an economy that is in the process of change.

What are the weaknesses of the Bolivian economy?

ER: Like any economy we have weaknesses. One is to do with access to finance. We don’t have deep capital markets or a stockmarket that can help us fund investment projects. Moreover, we have been hit by the increase in external financing costs. Two years ago, the Federal Reserve’s benchmark rate was 0.5%; it is now 5.5% and that is a massive difference that hits our country risk.

Bolivia’s dollar reserves have fallen; is that an economic threat?

ER: We need to differentiate between the stock of reserves and the liquidity of dollars. The stock has fallen because of a combination of external and internal factors. First, we had Covid-19. Then, during the middle of the pandemic, there was a coup d’état in Bolivia, which caused massive disruption. Finally, we were hit by the economic effects of the war in Ukraine, which increased the cost of the diesel and oil that we import. Meanwhile the output of our main export, natural gas fell, while our major market – Argentina – doesn’t pay us on time. All of that caused our reserve stock of dollars to fall.

Bolivia has huge reserves of lithium. Indeed, our lithium reserves have a value 75-times greater than our GDP, so the economic impact of developing them would be huge. Edwin Rojas, President of the Central Bank of Bolivia

But not all of the factors were negative. Our industrialisation process has encouraged the import of capital machinery, which reduces our stock of dollars but ultimately is good for growth. That’s why our industrial goods have had a trade surplus in the last two years. The most important thing to note is that we don’t have a problem with the availability of dollars, and Bolivia has been able to meet any of its dollar requirements. Moreover, we are using innovative mechanisms to increase our access to dollars. We are buying gold with local currency that we can later sell for dollars. In the long-run these gold operations will help us increase our dollar stock.

Over the last decade the Bolivian peso has been more stable against the dollar than the pound; why?

ER: We have a stable exchange rate thanks to the macroeconomic strengths that I mentioned earlier. But this is about more than just numbers – we have convinced people to believe in the local currency. When you look at the problems with the financial system earlier this year, we thought that Bolivians might rush to exchange bolivian currency for dollars, but it didn’t happen to any great extent.

This hasn’t been easy to achieve because there is a trauma in the national psyche caused by the hyperinflation of the 1980s, which is one of the most extreme cases of currency depreciation that ever happened. Some Bolivians still think that the US dollar is safer, which is ironic because this year the real value of the dollar has been eroded by 6% compared to just 2.7% for the Bolivian peso. Looking ahead, some of the new exports that are expected – ie lithium, zinc and gypsum – will shore up the Bolivian even more. We are also building a diesel substitution plant that will allow us to cut diesel imports.

Please share your vision of the Bolivian economy in 2030.

ER: The Central Bank of Bolivia will continue to expand our links with international financial institutions. We have good relationships with correspondent banks across the world, and work with the Central Bank of Spain for international payments. We are always keen to see more international players enter our financial system, and I recently travelled to China to encourage banks from that country to come to Bolivia. Looking at the economy in more general terms, we will see more import substitution by 2030. That will make us less susceptible to some of the external shocks that we have seen in recent years.

Thanks to our goals of targeting economic growth and redistribution, the economic purchasing power of the Bolivian people will have increased. The financial system will be as stable as ever, but probably much larger. We are keen to deepen our financial sector and develop capital markets because that will help us access better financing. The Bolivian economy in 2030 will be much more modern and sustainable than it is today.